Picture this: You grab a $6 fancy coffee every morning, but then scramble to cover rent or groceries at month’s end. It’s a classic mix-up between needs and wants that leaves many feeling stressed and broke. With food prices up 3.1% and rent steady at 3% higher year-over-year as of February 2026, these lines blur even more.

Needs keep you alive, like basic food, shelter, and clothes. Wants add comfort or joy, such as that latte or eating out. Spotting the difference helps you save cash, pay off debt faster, and build real wealth over time.

Rising costs make it tougher, yet simple shifts pay off big. In this post, you’ll get clear definitions, real-life examples, five key questions to test any purchase, common pitfalls to dodge, and budgeting tips that stick. Let’s start by breaking down what truly counts as a need.

What Makes Something a True Need in Your Daily Life

You know a need when skipping it leads to real trouble, like hunger, eviction, or illness. These basics protect your health and survival. They differ by your situation; a rural commuter might require a car, while city folks rely on buses. Experts agree you must fund needs first. Dave Ramsey stresses this in his guide on needs vs. wants, because covering them stops most money messes. Studies back it up. For instance, a CNBC report shows 29% of working households barely handle basics, leading to debt traps.

Consider this quick comparison to spot the line:

| Need | Similar Want |

|---|---|

| Groceries for meals | Eating out weekly |

| Basic rent or mortgage | Luxury apartment upgrade |

| Utility bills | Streaming subscriptions |

| Work clothes | Designer outfits |

| Bus pass or used car | New SUV |

Prioritizing the left column builds stability. Now, let’s look closer at survival must-haves.

Survival Essentials You Can’t Skip

Food tops the list, but stick to groceries, not gourmet treats. Groceries rose 2.4% in the year to February 2026, so buy rice, beans, eggs, and veggies for home cooking. Skip that without eating leads to weakness or health issues fast.

Housing means basic rent or a modest mortgage payment. Rent climbed 3.0% over the past year through February 2026. You need a roof; anything fancier risks eviction if cash runs low.

Utilities keep lights on and water flowing. Basic phone and internet help you work or call for help. Without them, you lose job access or face shutoffs. Cover these three first. Data shows folks who do avoid 80% of common financial slips, like overdrafts or loans.

Picture unpacking simple bags after work. That’s security.

Health and Mobility Basics That Keep You Functional

Healthcare checkups prevent small issues from exploding. Annual visits or meds keep you working. Skip them, and a cold turns costly.

Basic clothes suit your job; clean shirts and pants do the trick. Designer labels? Not if they strain your budget.

Transport gets you to work reliably. A bus pass or used car works fine. In contrast, your basic phone handles job calls, but the newest model with extras does not. Without reliable rides, you risk firing.

These tie straight to job security. Miss shifts from car trouble? Paychecks vanish. Fund them so you stay employed and steady. For example, a waitress needs sturdy shoes; flashy heels break ankles and shifts. Basics keep you moving forward.

Spotting Wants That Feel Essential But Aren’t

Wants boost your joy, but you can live without them. Think designer clothes or quick vacations. They motivate you, yet they must fit your budget after needs. Otherwise, they drain cash fast. Experts like debt attorney Leslie Tayne stress this point. She urges people to review past spending and treat wants as optional. In contrast, needs like groceries beat fancy dinners every time. Basic health checkups outrank gym memberships too. Apps in 2026 make control easier. They cap wants at 30% of your budget with alerts and tracking. PocketGuard or YNAB show safe spend amounts right away. So, you dodge overspending traps.

Fun Upgrades and Luxuries to Watch For

These extras feel vital until you skip them. A luxury apartment add-on, like smart lights or a gym membership in the building, tempts you. Designer brands promise status. Top-tier streaming packs every show. Yet, they pile up quick.

Take daily coffee. At $5 a cup, it hits $150 a month. Add a designer bag at $200 and premium streaming at $20. You reach $370 before lunch habits kick in. Basic coffee brews at home for pennies. Standard clothes work fine. Free streaming tiers cover hits.

Here’s how common ones stack against needs:

| Want Example | Monthly Cost Estimate | Need Counterpart |

|---|---|---|

| Luxury apartment extras | $50-100 | Basic rent |

| Designer brand outfits | $100-300 | Work-appropriate clothes |

| Top streaming bundles | $20-40 | Free or basic tiers |

| Daily fancy coffee | $150 | Home-brewed |

That cozy setup looks great. Still, it adds up. Cut back, and your savings grow.

Experiences and Hobbies That Enhance But Don’t Define Life

Travel sparks adventure. Hobbies relax you after work. Entertainment nights lift spirits. They enhance life, but life goes on without them. Split wants into fun and luxuries for better grip. Fun covers cheap outings. Luxuries mean big trips.

A weekend getaway costs $500. Golf lessons run $100 monthly. Concert tickets top $150. These beat boredom, yet home workouts or park walks fill gaps. Local hikes replace flights. Free podcasts swap paid shows.

Subdividing helps. Assign 15% to fun experiences and 15% to luxuries. Apps track it live. You get warnings before overspend. As a result, hobbies stay joyful, not stressful. Needs stay safe too. After all, memories matter, but so does your bank account.

Easy Tests to Decide Need or Want Before You Buy

You face a purchase decision every day. So, how do you know if it’s a true need or just a nice-to-have? These quick tests clear the fog right away. They take seconds to run, yet they save you hundreds. Best of all, you can use them anywhere, from the store aisle to online carts. Let’s jump into the questions first, then see them in action.

Five Questions That Cut Through the Confusion

Grab a notepad or your phone notes app. Ask these five questions before any buy. Answer honestly each time. They reveal the truth fast.

- Can I survive without it? Needs keep you safe and healthy. Wants add fun. For example, you need basic groceries. However, that $6 latte? Skip it, and you still eat. Brew coffee at home for pennies instead.

- Is there a cheaper option that works? Check basics first. A used car at around $25,000 gets you to work reliably. Yet, a new luxury model over $50,000? It shines, but the beater does the job.

- Does it help my big goals? Think debt payoff or savings. A gym membership might fit if you aim for health. Still, free park runs push the same goals without cost.

- Would I need it if my income dropped? Picture job loss or cuts. Essentials stay. Internet for job hunts? Yes. Latest streaming bundle? No, basics or library Wi-Fi cover it.

- Am I okay without it tomorrow? Delay tests impulse. Crave new shoes now? Wait a day. If the urge fades, it’s a want.

Test them now. Pull your last bank statement. Spot one or two buys, like takeout or apps. Reclassify them. That coffee run? Home brew wins. This habit stops debt before it starts. Sites like How to Money’s buy-it checklist back these steps with real user wins.

Ponder like this, and regrets drop.

Watch pitfalls too. People label wants as needs, like calling cable “utilities.” Emotional buys hit after stress. These questions block that. As a result, your wallet stays full.

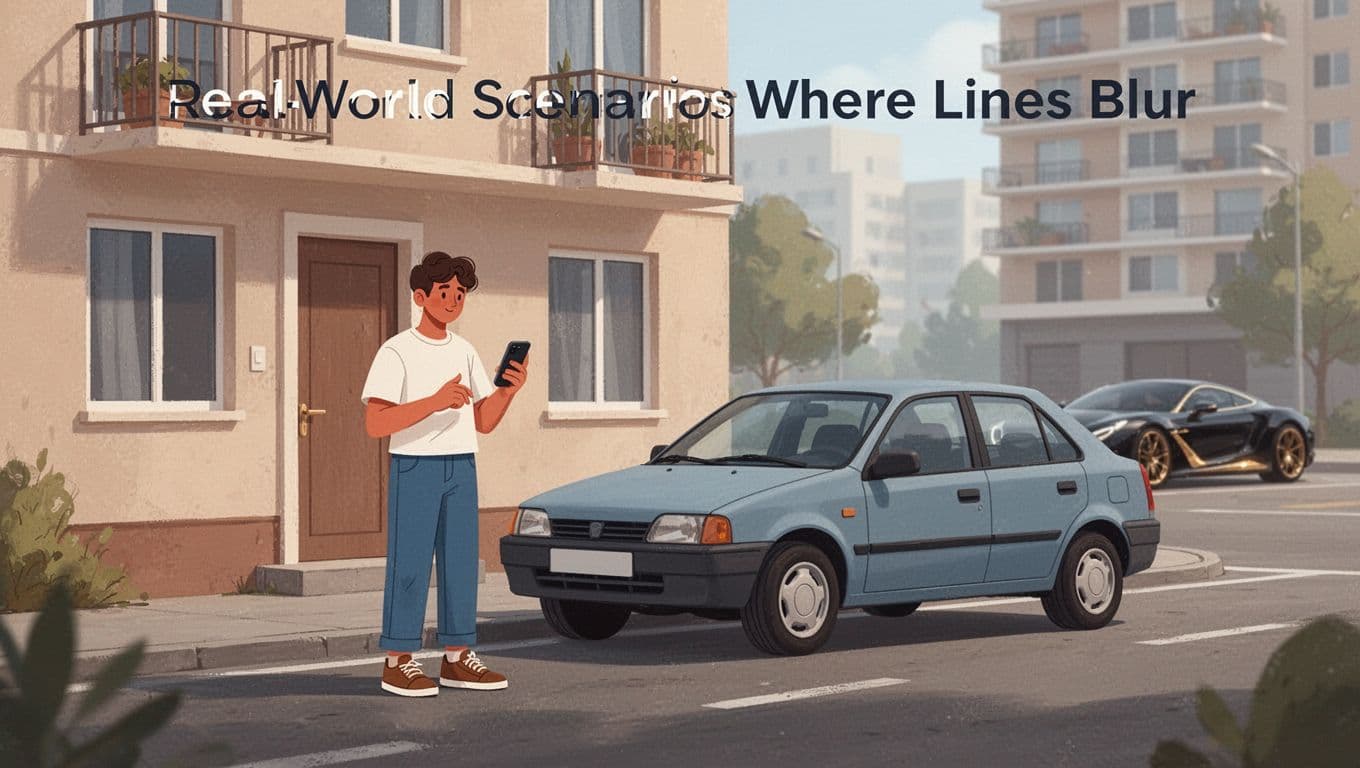

Real-World Scenarios Where Lines Blur

Situations shift the line between need and want. Your job, location, or family change everything. Let’s break down cars, phones, and rent.

Start with cars. A rural worker needs reliable wheels for shifts. A basic used one at $25,000 fits. However, city buses make that a want. Luxury new rides top $50,000. They impress, yet basics get you there. If rideshares work cheap, skip the car altogether.

Phones work the same. Everyone needs basic calls and texts for work or emergencies. A simple model handles it. The latest iPhone packs cameras and apps. Great for influencers, but overkill for most. Test it: Does your current phone fail core tasks? If not, upgrade waits.

Rent blurs most. Basic apartments cover shelter. Add a view, and costs jump. You pay for sunsets, not survival. Families might need space over views. Singles in walkable spots? Views tempt less. Check your musts first.

These examples show context rules. Run the questions each time. Your answers adapt to life. In short, stay flexible, and money flows to what counts.

Basics like these keep choices clear.

Balance Your Budget with Needs First and Smart Rules

You have sorted needs from wants. Now put that knowledge to work in your budget. Start with needs, cap wants, and save the rest. This approach builds stability fast. Rising costs in 2026 make it essential. Food and rent keep climbing, so smart rules help you stay ahead. For example, the popular 50/30/20 rule guides many Americans. It splits your after-tax income simply. Yet, experts note you must tweak it for high living expenses.

Master the 50/30/20 Rule for Financial Freedom

The 50/30/20 rule divides your take-home pay clearly. Put 50% toward needs like rent, groceries, and bills. Next, 30% covers wants such as dining out or movies. Finally, 20% goes to savings or debt payoff. This method gained huge traction in 2026. TikTok videos rack up millions of views, and it tops searches for beginners. However, inflation pushes needs over 50% for some, so adapt as needed.

Take a $4,000 monthly income. That means $2,000 for needs, $1,200 for wants, and $800 for savings. You cover basics first. Then enjoy some fun without guilt. Savings grow steadily. As a result, you build an emergency fund.

This pie chart shows the split at a glance. Simple icons make it stick.

See Investopedia’s breakdown for more examples. People love it because no complex math required. Still, cap wants amid rising costs. Otherwise, savings vanish. Experts like those at WalletHub say include some wants. They prevent burnout. Skip fun entirely, and you quit budgeting fast.

Track and Trim to Avoid Common Traps

Tracking reveals hidden leaks. Many overspend on variable costs like eating out. Others skip savings buffers, then face emergencies broke. No buffer means credit card debt. As a result, stress builds quick.

Start by listing expenses weekly. Apps make it easy. Top picks like those in NerdWallet’s 2026 review auto-track and alert overspends. They categorize needs versus wants too. In addition, negotiate bills often. Call your cable or internet provider. Mention competitors’ deals. You save $10 to $25 monthly easy. Check NerdWallet’s negotiation guide for scripts that work.

Choose cheaper alternatives next. Brew coffee at home instead of $6 lattes. Shop store brands for groceries. These swaps fit wants under 30%. However, avoid too-strict budgets. They fail 97% of the time from frustration. Balance keeps you going.

Common pitfalls include calling subscriptions “needs.” Build that buffer first. Then enjoy life. Audit your budget today. Pull statements, apply 50/30/20, and trim one item. You gain control right away.

Conclusion

You now know how to spot needs from wants with those five quick questions. They cut through confusion fast. Use the 50/30/20 rule next. Put 50% on needs first, then enjoy 30% on wants, and save 20%. As a result, stress drops and savings grow.

Small swaps make big wins. Ditch that daily latte for home brew. Watch your bank account build instead. These steps lead to real freedom, even with rising food and rent costs.

List your top three spends today. Classify each as need or want. Share in the comments below. What changed for you?